Most retirees have Medicare Part B premiums deducted directly from their Social Security payments through Centers for Medicare & Medicaid Services.

If Part B premiums rise in 2026, they may absorb part of your COLA.

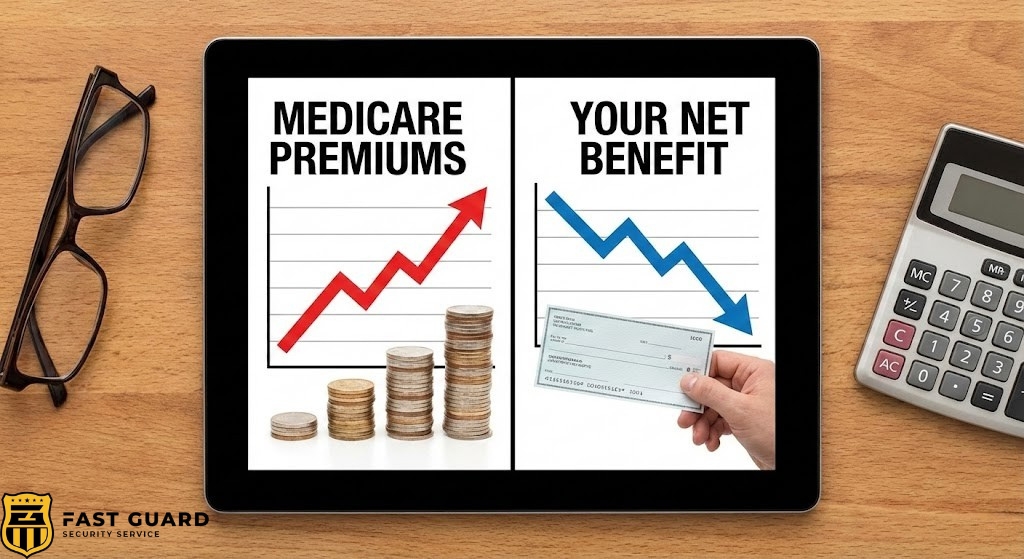

Example:

- $56 COLA increase

- $20 premium increase

- Net gain = $36

For retirees on fixed incomes, always calculate net, not gross, benefit changes.

Retirement Age Rules Still Matter

Your claiming age remains one of the biggest lifetime income decisions.

- Claim at 62 → Permanently reduced benefits

- Claim at Full Retirement Age (FRA) → Unreduced benefits

- Claim at 70 → Maximum monthly benefit via delayed retirement credits

Age thresholds did not change in 2026, but the dollar amounts increased due to COLA.

Delaying benefits can increase lifetime income far more than a single annual COLA.

Earnings Limits for Working Beneficiaries (2026)

If you claim benefits before FRA and continue working, earnings limits apply.

In 2026:

- $24,480 annual limit (under FRA)

- $65,160 limit (year you reach FRA)

If you exceed the limit:

- The SSA temporarily withholds part of your benefits

- Those benefits are not permanently lost

- Your monthly payment is recalculated at FRA

Income planning remains especially important for early retirees transitioning out of the workforce.

Payroll Taxes, Work Credits, and Eligibility

Social Security is funded through payroll taxes under the Old-Age, Survivors, and Disability Insurance (OASDI) program.

In 2026:

- Maximum taxable earnings: $184,500

- Earnings above that amount are not subject to Social Security tax.

This means:

- Higher earners pay Social Security taxes on a larger portion of income

- Future benefit calculations may be slightly affected

- System funding improves modestly

To earn one work credit in 2026, you must earn $1,890.

You can earn up to four credits per year.

What Is the Maximum Social Security Benefit in 2026?

The maximum Social Security benefit in 2026 depends on your claiming age and lifetime earnings. Workers who consistently earned at or above the taxable maximum ($184,500 in 2026) and delay benefits until age 70 qualify for the highest possible monthly payment.

Those who claim at Full Retirement Age receive a lower maximum, and claiming at age 62 reduces the benefit further. Because benefits are calculated using your highest 35 years of earnings, reaching the maximum requires both high lifetime income and strategic timing.

Survivor and Spousal Benefits

Social Security also provides protection for families:

- Survivor benefits support dependents after a worker’s death

- Spousal benefits can equal up to 50% of the primary earner’s FRA benefit

- The 2.8% COLA applies to these payments as well

For single-income households, these benefits remain a major layer of financial security.

How These Changes Work Together

The system operates as a formula:

Inflation → Determines COLA

Wage growth → Adjusts earnings limits & taxable caps

Payroll taxes → Fund future benefits

Medicare premiums → Affect net deposits

Because these elements interact, a headline COLA percentage never tells the whole story.

What You Should Do in 2026

Proactive planning can increase lifetime income.

- Review your earnings record through your SSA account

- Run benefit estimates at ages 62, FRA, and 70

- Model net payments after Medicare deductions

- Consider working income limits if claiming early

- Coordinate claiming with your spouse

Small timing decisions can permanently affect thousands of dollars over retirement.

Final Thoughts

Social Security changes in 2026 affect nearly every beneficiary through the confirmed 2.8% COLA, updated earnings limits, higher taxable income caps, and Medicare interactions.

While the system may seem complex, each adjustment follows predictable formulas based on inflation and wage growth.

Staying informed, and planning strategically, helps protect your income and ensures confident financial decisions for the year ahead.